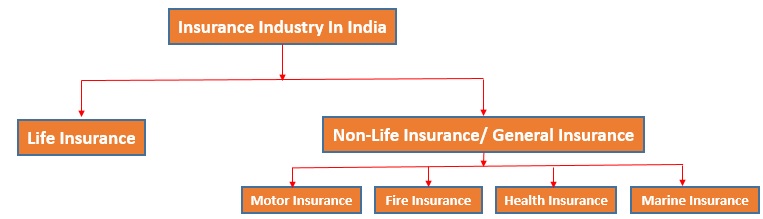

Insurance Industry comprises mainly two players : Life Insurers and General Insurers

Life Insurer

Under Government Control LIC is the only Life Insurer.

Types of Life Insurance in India

- Term Life Insurance – It is life insurance that provides coverage only if the insured dies during the period specified in the policy; that specified period is known as the policy term. A life insurance policy’s face amount is the amount of life insurance benefits for which an individual applies and that the insurer approves.

- Whole Life Insurance – It is a type of cash value life insurance that provides lifetime insurance coverage, usually at a level premium rate that does not increase as the insured ages.

- Universal Life Insurance – It is a form of cash value insurance that is characterized by its separation of the three primary policy elements (mortality charges, interest rate, expenses) and its flexible face amount and premiums.

- Variable Life Insurance – It is also a form of cash value life insurance in which premiums are fixed but the death benefit and other values may vary, reflecting the performance of the investment sub-accounts that the policy owner selects.

- Endowment Insurance – It provides a specified benefit amount whether the insured lives to the end of the term of coverage or dies during that term.Each endowment policy specifies a maturity date, which is the date on which the insurer will pay the policy’s face amount to the policy owner if the insured is still living.

Life Insurance Policy

Term Insurance Policies : The policy holder does not get any monetary benefit at the end of the policy term except for the tax benefits he or she can choose to avail of throughout the tenure of the policy. In the event of death of the policy holder, the sum assured is paid to his or her beneficiaries.

Endowment Policies : An endowment policy is a life insurance contract designed to pay a lump sum after a specific term (on its ‘maturity’) or on death. Typical maturities are ten, fifteen or twenty years up to a certain age limit. Fer standard plans as follows:

- Money-back Policies – Money back policies are basically an extension of endowment plans wherein the policy holder receives a fixed amount at specific intervals throughout the duration of the policy. In the event of the unfortunate death of the policy holder, the full sum assured is paid to the beneficiaries.

- Unit-linked Investment Policies (ULIP) : Unit linked insurance policies again belong to the insurance-cum-investment category where one gets to enjoy the benefits of both insurance and investment. While a part of the monthly premium pay-out goes towards the insurance cover, the remaining money is invested in various types of funds that invest in debt and equity instruments. ULIP plans are more or less similar in comparison to mutual funds except for the difference that ULIPs offer the additional benefit of insurance.

- Pension Policies : Pension policies let individuals determine a fixed stream of income post retirement.

General Insurers

Any insurance other than ‘Life Insurance’ falls under the classification of General Insurance. It comprises of :

- Insurance of property against fire, theft, burglary, terrorism, natural disasters etc.

- Personal insurance such as Accident Policy, Health Insurance and liability insurance which covers legal liabilities.

- Errors and Omissions Insurance for professionals, credit insurance etc.

- Policy covers such as coverage of machinery against breakdown or loss or damage during the transit.

- Policies that provide marine insurance covering goods in transit by sea, air, railways, waterways and road and cover the hull of ships.

- Insurance of motor vehicles against damages or accidents and theft.

All these above mentioned form a major chunk of non-life insurance business.

In the Government Control, General Insurance Corporation of India (GIC) (with effect from Dec’2000, a National Re-insurer) GIC had four subsidiary companies, namely

i). The Oriental Insurance Company Limited

ii). The New India Assurance Company Limited

iii). National Insurance Company Limited

iv). United India Insurance Company Limited

(With effect from Dec’2000, these subsidiaries have been de-linked from the parent company and made as independent insurance company)

Insurance Sector In India is governed by

The Insurance sector in India is governed by Insurance Act, 1938, the Life Insurance Corporation Act, 1956 and General Insurance Business (Nationalization) Act, 1972, Insurance Regulatory and Development Authority of India (IRDAI) Act, 1999 and other related Acts. With such a large population and untapped market area of this population, insurance happens to be a very big opportunity in India.

Today it stands as a business growing at the rate of 15-20 percent annually. Together with banking services, it adds about 7 percent to the country’s GDP. In spite of all this growth, the statistics of the penetration of the insurance in the country is very poor. Nearly 80% of Indian populations are without Life insurance cover and the Health insurance. This is an indicator that growth potential for the insurance sector is immense in India.

It was due to this immense growth that the regulations were introduced in the insurance sector and in continuation “Malhotra Committee” was constituted by the government in 1993 to examine the various aspects of the industry. The key element of the reform process was participation of overseas insurance companies with 26% capital. Creating a more efficient and competitive financial system suitable for the requirements of the economy was the main idea behind this reform.

Since then the insurance industry has gone through many sea changes. The competition that LIC started facing from these companies were threatening to the existence of LIC. Since the liberalization of the industry, the insurance industry has never looked back and today stand as the one of the most competitive and exploring industry in India. The entry of the private players and the increased use of the new distribution are in the limelight today. The use of new distribution techniques and the IT tools has increased the scope of the industry in the longer run.

Life Insurance In United State of America (USA)

All the best for your upcoming exam!

You can join or visit at Facebook Page or Twitter for always keep in touch with further updates.

Read more articles….